Have you ever checked your car insurance bill and wondered, “Why does my car insurance go up every 6 months?” You’re not alone. Many drivers feel frustrated when their rates climb without a clear reason.

Understanding why this happens can help you take control and possibly save money. You’ll discover the real factors behind those rising costs and what you can do about them. Keep reading to stop feeling surprised every time your bill arrives.

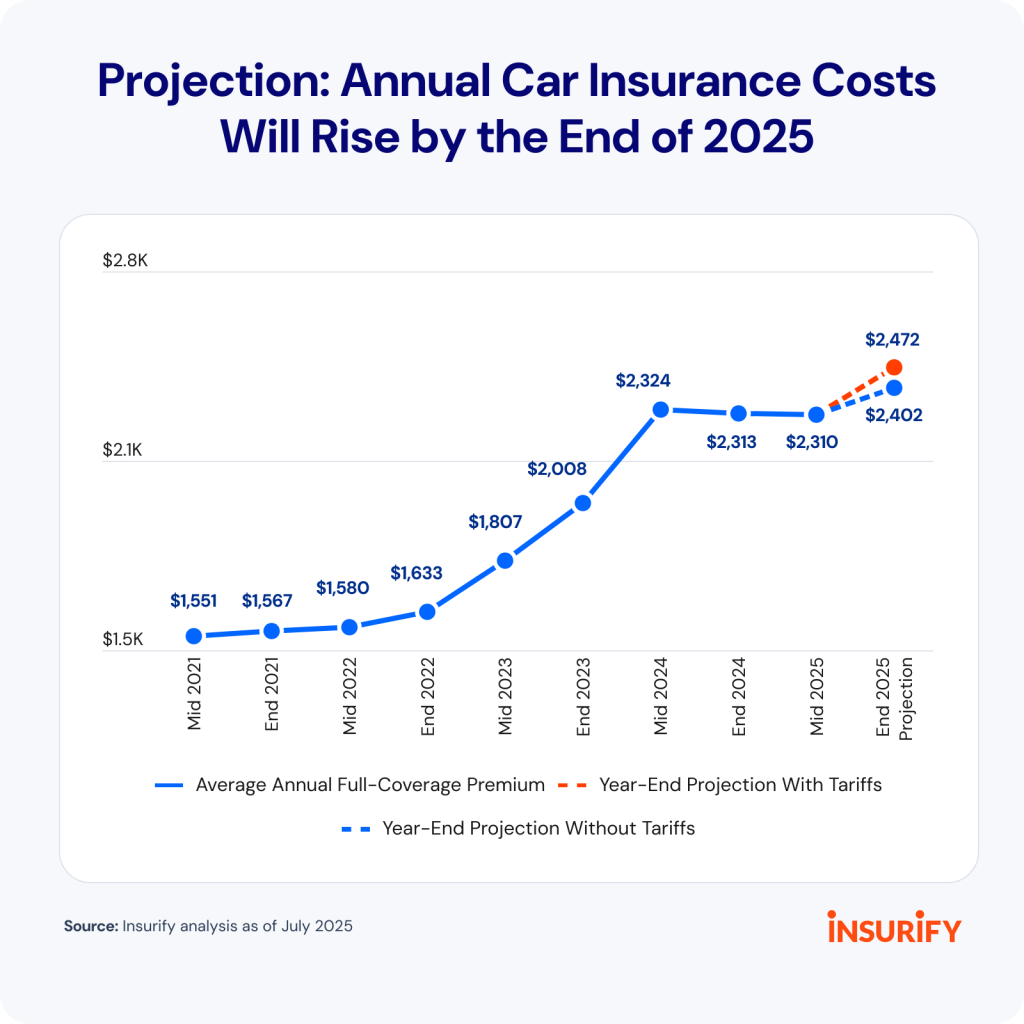

Credit: www.nerdwallet.com

Factors Driving Biannual Rate Increases

Understanding why your car insurance premiums rise every six months can feel frustrating. Several key factors influence these biannual increases, shaping how insurers adjust your rates. Knowing these elements can help you anticipate changes and take control of your insurance costs.

Claims History Impact

Your own claims history plays a major role in how much your insurance costs. If you’ve filed claims recently, insurers see you as a higher risk, which often leads to higher premiums. Even a minor accident or a glass repair claim can signal increased risk to your provider.

Think about it: have you noticed a jump in your rates after a claim? This connection means your driving record isn’t just about tickets; it’s about any insurance activity that shows potential for future claims.

Regional Accident Trends

Where you live affects your insurance rates more than you might expect. If your area experiences more accidents, thefts, or natural disasters, insurers adjust premiums to cover those risks. Even if you’re a safe driver, regional trends can push your rates up.

Consider this: have your neighbors’ driving habits or local traffic conditions changed? These shifts can create a ripple effect, influencing your insurance costs without any change in your personal record.

Insurance Company Profit Goals

Insurance companies are businesses aiming to stay profitable. If overall claims exceed expectations, companies may raise rates to balance their books and maintain profits. This means your premiums can increase simply because the insurer needs to cover rising costs.

Ask yourself: how much control do you have over the company’s financial goals? While you can manage your risk, market-wide profitability drives many rate changes beyond individual behavior.

Role Of Your Driving Record

Your driving record plays a crucial role in determining why your car insurance might increase every six months. Insurers view your history behind the wheel as a direct indicator of risk. The cleaner your record, the better your chances of keeping premiums low.

Effect Of Minor Violations

Minor violations like rolling through a stop sign or failing to signal can still impact your insurance rates. These small mistakes suggest to insurers that you may be a higher risk than a perfectly clean driver. Even if you haven’t been in an accident, repeated minor infractions can add up and lead to a premium increase.

Think about the last time you got a warning for something small. Did your insurance change afterward? It might not be immediate, but these violations are often tracked over time and influence your rates during renewal.

How Accidents Affect Premiums

Accidents are one of the most significant factors that cause your insurance to rise. Whether you were at fault or not, an accident can signal to the insurer that you might file claims more frequently. This increased perceived risk usually results in higher premiums at your next policy renewal.

Consider a situation where you had a minor fender bender but didn’t claim it. Even without a claim, the accident might appear on your record and affect your rates. Insurers often access detailed driving histories that include reported accidents.

Influence Of Traffic Tickets

Traffic tickets are a clear red flag to insurance companies. Tickets for speeding, running red lights, or reckless driving indicate risky behavior. These tickets can cause your insurance to jump when it’s time for renewal.

Not all tickets affect your premium equally. A speeding ticket might increase your rate less than a reckless driving citation. But multiple tickets, even minor ones, can stack up and cause significant premium hikes.

Have you ever wondered if paying a fine quickly or attending traffic school helps? Sometimes, these actions can reduce the impact on your insurance. It’s worth checking if your insurer offers discounts for such measures.

Changes In Vehicle Value And Repair Costs

Car insurance rates often rise because of changes in vehicle value and repair costs. These factors directly affect how much insurers must pay after an accident. When repair costs increase, insurers charge more to cover these expenses. The value of your car also changes over time, influencing your premium. Understanding these elements helps explain why your insurance might go up every six months.

Rising Repair Expenses

Repair costs for cars grow steadily. Labor charges are higher now than before. New technology in vehicles makes repairs more complex. This complexity means more time and skill are needed. More parts might need replacement instead of repair. All these add to the total repair bill.

Impact Of Vehicle Age

Older cars lose value but may cost more to fix. Parts for older models are harder to find. Insurers adjust premiums to match these costs. Some older cars need special repairs that take longer. This raises the cost of claims for insurance companies.

Parts Availability And Costs

Parts availability plays a big role in repair costs. Rare or discontinued parts cost more to buy. Shipping and sourcing special parts add to expenses. Insurers factor these costs into your premium. The harder it is to find parts, the higher the insurance rate.

Credit: www.reddit.com

External Economic And Environmental Factors

Car insurance rates often rise every six months due to factors beyond your control. External economic and environmental influences play a big role in these changes. Insurance companies adjust premiums based on risks they face from the economy and nature.

These factors can increase the cost of claims and the overall expense for insurers. As a result, your premium goes up to cover these higher costs. Understanding these reasons helps you see why your insurance bill changes regularly.

Inflation And Its Effect

Inflation raises the price of goods and services. Repair costs for cars get higher as parts and labor become more expensive. Insurance companies must pay more to fix damages.

This increase in costs makes insurers raise premiums. They need to keep up with the rising expenses. Inflation also affects medical bills after accidents, increasing claim amounts.

Weather-related Claims Increase

Extreme weather events cause many insurance claims. Storms, floods, and hail damage cars frequently. The number of claims rises during bad weather seasons.

Insurance companies pay more for these damages. They adjust rates to cover the growing risk. Areas with more natural disasters often see bigger premium hikes.

Legal And Regulatory Changes

New laws can affect insurance costs. Rules about minimum coverage or claim handling may change. Insurers must follow these laws, which can increase their expenses.

Legal changes can also lead to more lawsuits or higher settlements. These risks push insurance companies to raise premiums. Staying compliant costs money that insurers pass to customers.

How Insurance Companies Adjust Rates

Understanding how insurance companies adjust rates can help you make sense of why your car insurance premiums might rise every six months. These adjustments are not random; they reflect ongoing changes in risk and data that insurers collect about you and the broader market. Knowing what influences these changes gives you a better chance to manage your costs.

Risk Assessment Updates

Insurance companies constantly update their view of your risk profile. They consider factors such as your driving record, claims history, and even changes in where you live. If you recently had a minor accident or a speeding ticket, your risk level might have increased, leading to higher rates.

Beyond your personal information, insurers also track trends like accident rates in your area or the rise in thefts. These external factors can affect your premium even if your driving habits haven’t changed. Have you noticed your neighborhood becoming busier or more prone to accidents? That could be why your rates are going up.

Use Of Telematics And Data

Many insurers now use telematics devices or apps to monitor your driving behavior. This data shows how fast you drive, how sharply you brake, and even the times you’re on the road. If your driving style is risky, your insurer might increase your premium when they review this data.

On the flip side, if you drive safely and avoid high-risk times like late nights, telematics can help lower your rates. Are you aware that simply driving more during rush hours or on highways can affect your premium? Your everyday choices behind the wheel can make a big difference in your insurance cost.

Frequency Of Rate Reviews

Insurance companies don’t wait for your policy to expire to review your rates. Many perform rate checks every six months to reflect the most current information. This frequent review helps them stay competitive and accurate in pricing, but it can also mean more frequent changes to your premium.

Think about it: if your insurer updated your rates only once a year, you might miss out on savings or not realize when your risk has increased. Does your current insurer provide clear updates on what causes rate changes during these reviews? Staying informed can help you challenge or adjust your coverage as needed.

)

Credit: insurify.com

Steps To Control Premium Increases

Controlling car insurance premium increases requires active effort. Understanding how to manage factors that affect rates helps keep costs down. Small changes can lead to noticeable savings over time.

Focus on habits, coverage choices, and comparing offers. Each area offers ways to reduce your insurance expenses effectively.

Improving Driving Habits

Safe driving reduces accident risk and insurance claims. Avoid speeding, harsh braking, and distracted driving. Keeping a clean driving record shows insurers you are low risk. Use apps or devices that track your driving behavior. Some insurers offer discounts for good driving scores.

Choosing The Right Coverage

Select coverage that fits your needs without extras. Remove unnecessary add-ons that increase your premium. Consider higher deductibles to lower monthly costs. Review your policy yearly to adjust coverage as your situation changes. Tailored coverage avoids overpaying for protection you don’t need.

Shopping Around For Better Rates

Compare quotes from different insurance companies regularly. Rates vary widely between providers for the same coverage. Use online tools or contact agents directly to gather offers. Switch providers if you find better rates with similar benefits. Staying loyal may not always save money.

Frequently Asked Questions

Why Does Car Insurance Increase Periodically?

Car insurance rates can rise due to several factors. Insurers may adjust rates based on inflation, increased claims, or changes in your driving record. Additionally, external factors like natural disasters or economic shifts can impact costs. Regular evaluations help insurers maintain profitability and manage risk effectively.

What Factors Affect Car Insurance Premiums?

Car insurance premiums depend on various factors, including your driving record, location, vehicle type, and coverage level. Age, gender, and credit score can also influence rates. Insurers assess these elements to determine risk and set appropriate premiums, ensuring they cover potential claim costs.

Can My Driving Record Impact Insurance Costs?

Yes, your driving record significantly impacts insurance costs. A clean record often results in lower premiums, while accidents or violations can increase rates. Insurers view a good driving history as less risky, offering discounts. Conversely, a poor record indicates higher risk, leading to higher premiums.

How Does Inflation Affect Car Insurance?

Inflation can increase car insurance rates as it raises costs for vehicle repairs, medical care, and other claim-related expenses. Insurers adjust premiums to cover these rising costs, ensuring they remain financially stable. Consequently, policyholders may see periodic increases in their insurance rates.

Conclusion

Car insurance rates often rise every six months for several reasons. Changes in your driving record or claims can affect your price. Insurance companies also adjust rates based on market trends and risk factors. Staying informed helps you understand these increases better.

Regularly comparing quotes can save you money. Keep your driving clean and update your insurer about any changes. This way, you control your insurance costs more effectively. Understanding why rates change makes managing your policy easier.